The Impact of AI on Private Equity

By Lee Sanderson | February 2026

/ebook_The%20Impact%20of%20AI%20%20on%20Private%20Equity/EN_The%20Impact%20of%20AI%20on%20Private%20Equity_illu.png?width=300&height=262&name=EN_The%20Impact%20of%20AI%20on%20Private%20Equity_illu.png)

Executive Summary

Artificial Intelligence (AI) is no longer a future-tense technology; it is a present-day force actively reshaping the entire investment landscape, presenting both profound opportunities and existential threats.

.png?width=663&height=499&name=Graphic_Use%20of%20AI%20(2).png)

This technology is a source of profound operational efficiency, but also a primary driver of competitive disruption and margin erosion. The nature of this risk can vary.

For “AI-native” companies, which are businesses founded specifically to solve a problem using AI where the technology is the core product, the main threat is algorithmic competition. This means they risk being out-innovated by a rival that develops a superior model, better data, or a more efficient AI architecture. Their entire business depends on the performance of their AI.

Conversely, for “AI-Adapter” companies that are integrating AI into existing products and workflows to gain efficiencies or add features, the risk is margin compression and commoditisation. Their challenge is not to build the best AI, but to use it to defend their market share as AI makes their core services cheaper and faster to replicate, while also capitalising on competitors that are slow to meet customer demand for AI-powered products or features.

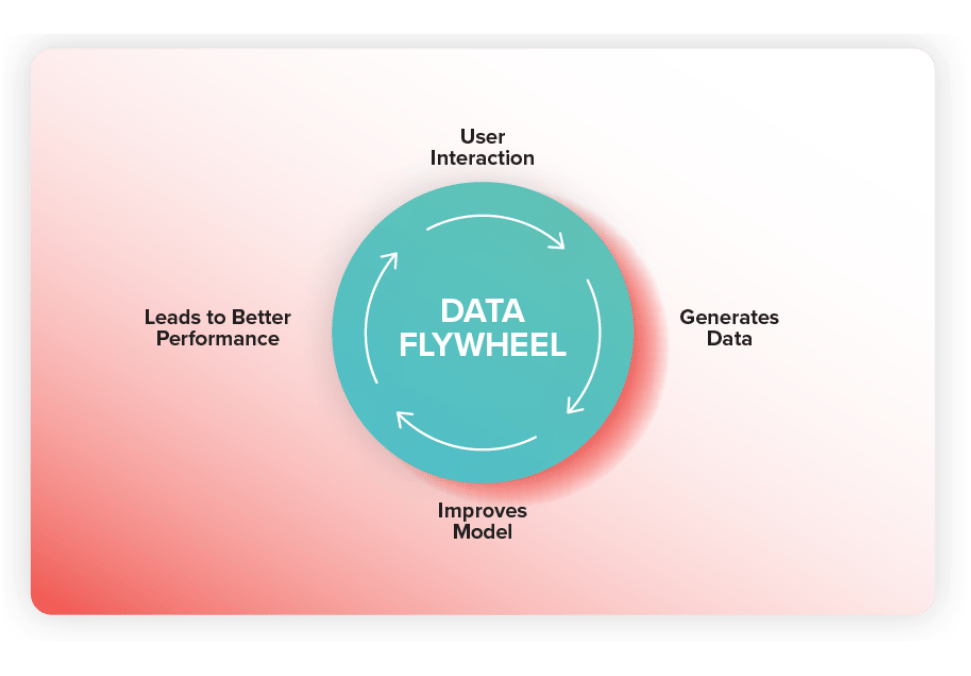

Competitive advantage can no longer rely on product features alone. Companies must build a sustainable barrier that protects them from competitors and the rapidly evolving AI landscape. These durable, defensible moats are strengthened by several factors, but one of the most critical is the creation of proprietary data flywheels. These are self-reinforcing systems where user activity generates unique data that improves the AI model, enhances the product, and attracts more users. When combined with deep integration into customer workflows, trust earned through transparent and explainable AI, and the strategic use of regulation to establish barriers to entry, these elements together create a lasting and resilient competitive edge.

Authored by Lee Sanderson, Principal Software Craftsperson at Codurance, this white paper provides a strategic framework for private equity investors, operating partners, and portfolio leaders navigating the AI revolution. It outlines the new competitive dynamics introduced by AI, details strategies for building durable and defensible moats, and presents a redefined playbook for the PE investment lifecycle – from initial diligence through to post-investment value creation and exit.

As a global software consultancy specialising in helping private equity-backed businesses unlock and accelerate value through modern technology, Codurance works across the investment lifecycle to modernise legacy systems, enable AI readiness, and build high-performing engineering teams. By bridging the gap between high-level investment strategy and deep technical execution, we help firms mitigate risk and realise stronger returns at exit.

Building Defensibility in the AI Era

As simple software features become commoditised, traditional moats based on functionality alone are eroding. The most durable and valuable moats in the age of AI are multifaceted, requiring a layered defence by combining proprietary data, deep technological integration, and a strong market position built on trust.

The Primacy of Proprietary Data

The apex of modern defensibility is the “data network effect”, or data flywheel. This is a virtuous cycle where a product’s use generates unique, proprietary data that no competitor can access. This data is then used to train and improve the underlying AI model. A better, smarter model leads to a superior product, which in turn attracts more users. These new users generate even more data, further accelerating the leader’s advantage and making the gap between them and their competitors increasingly difficult to close. This is the ultimate moat.

Trust and “Explainable AI”

In high-stakes verticals such as finance, law, compliance, and healthcare, trust is a fragile prerequisite for adoption. A company that can offer explainable AI, providing a clear, auditable trail for why its AI made a specific recommendation, gains a powerful competitive advantage over opaque black box systems, which carry significant reputational and legal risk. Auditability is not a feature but a core requirement.

Niche Market Specialisation

For companies facing existential threats from large, generalist platforms, the most viable defence is to become the undisputed expert in a specific vertical or workflow. This deep focus allows them to build features, models, and integrations trained on domain-specific terminology, regulations, and processes that broader, general-purpose AI systems are not optimised to interpret with the same level of precision.

The gap between leaders with a functioning data flywheel and laggards is becoming insurmountable. Are your portfolio companies building moats or just features? Codurance helps you design and implement the ‘Data-to-Product’ pipelines necessary to turn user interaction into a compounding competitive advantage.

Regulation as a Competitive Barrier

An emerging and powerful moat is the strategic use of complex regulations. The increasing complexity of the regulatory landscape, particularly the EU AI Act, can be turned into a competitive advantage. Companies whose tools may be classified as “High-Risk” (e.g., in HR, finance, or critical infrastructure) can build a “compliance moat”. By proactively achieving and marketing adherence to these stringent standards, they create a significant barrier to entry for new or less-prepared competitors, turning a regulatory burden into a marketable asset.

Deep Workflow Integration

This strategy, while not specific to AI, reflects a traditional but highly effective approach to building defensibility. When a product is deeply embedded into a customer’s critical and complex business processes, such as becoming the system of record for accounting, the core platform for logistics, or the central hub for HR, the cost, difficulty, and operational risk of replacing it become immense. This creates powerful customer lock-in and extremely high switching costs.